(AsianFin)— In 2023, U.S. companies released a total of 109 basic models, more than five times the number released by Chinese peers, according to the seventh annual Artificial Intelligence (AI) Index Report released by Stanford University’s Human-Centred Artificial Intelligence.

AI is catching up with humans, and polls show that 52% of people are more concerned than excited, said the report.

Compared with Chinese AI developments, the U.S. AI industry demonstrates significant advantages in the number of AI basic model releases and investment activities.

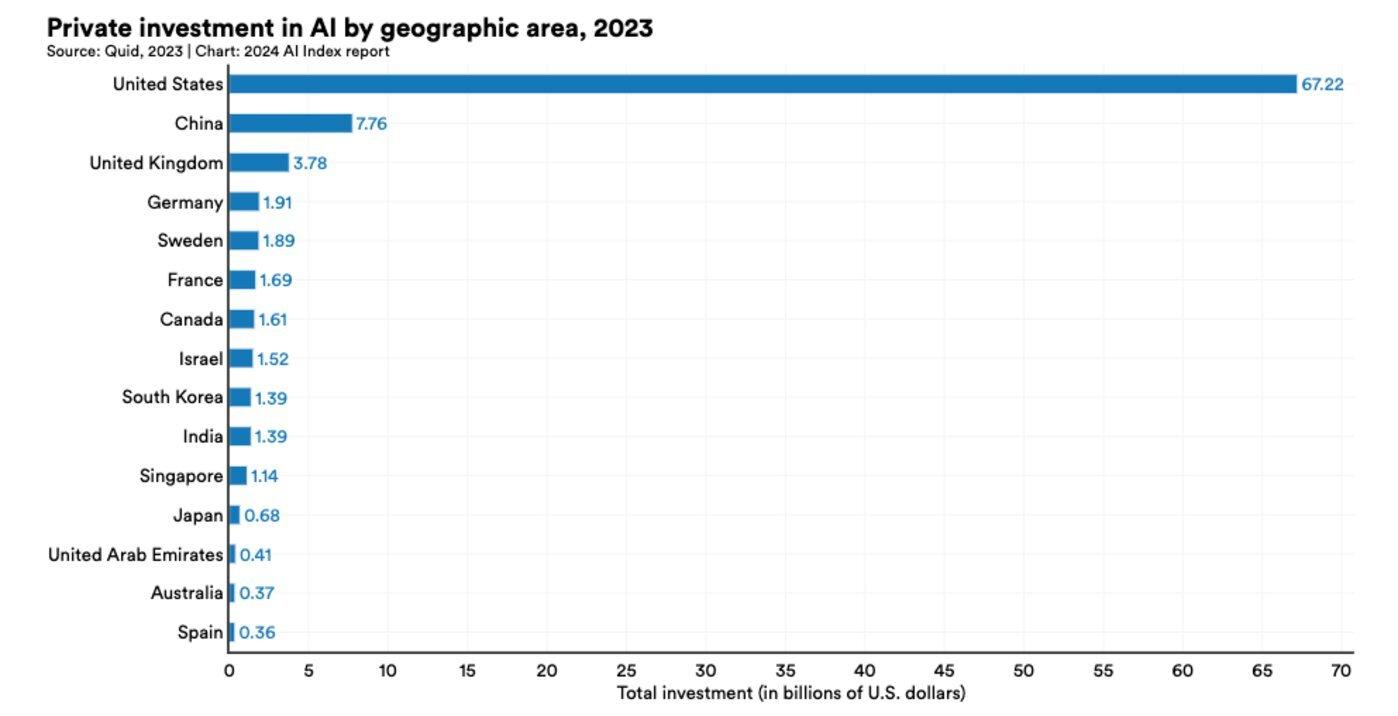

Meanwhile, the U.S. AI industry's investment in 2023 reached $67.2 billion, 8.7 times that of China’s $7.8 billion. Additionally, the U.S. had 61 well-known AI large models, while China had only 15.

Top 10 takeaways from the report are as follows:

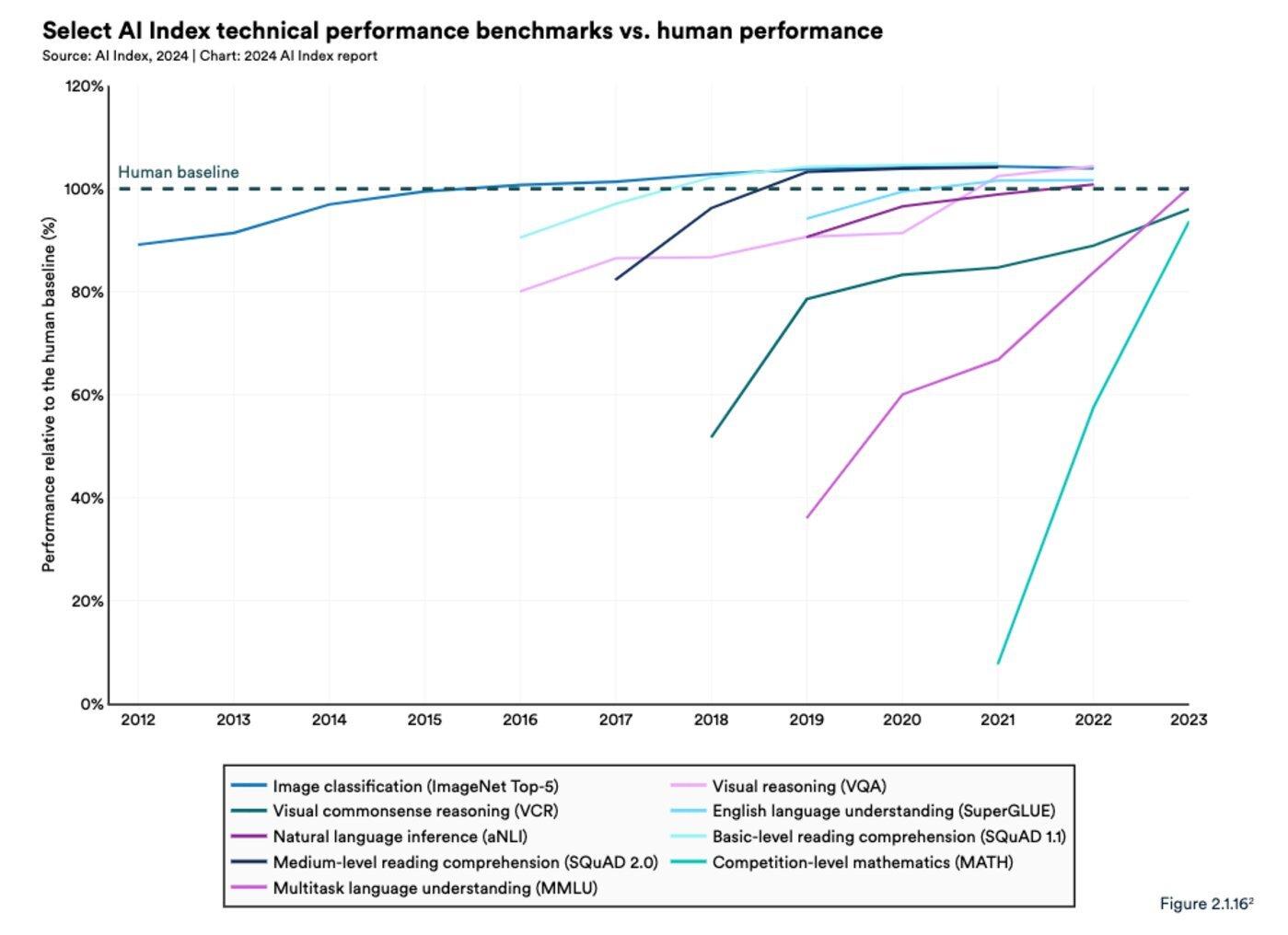

1. AI beats humans on some tasks, but not on all.

AI outperforms humans on image classification, visual reasoning and English understanding benchmarks, but it is not as good at more complex tasks such as competition-level mathematics, visual commonsense reasoning, and planning.

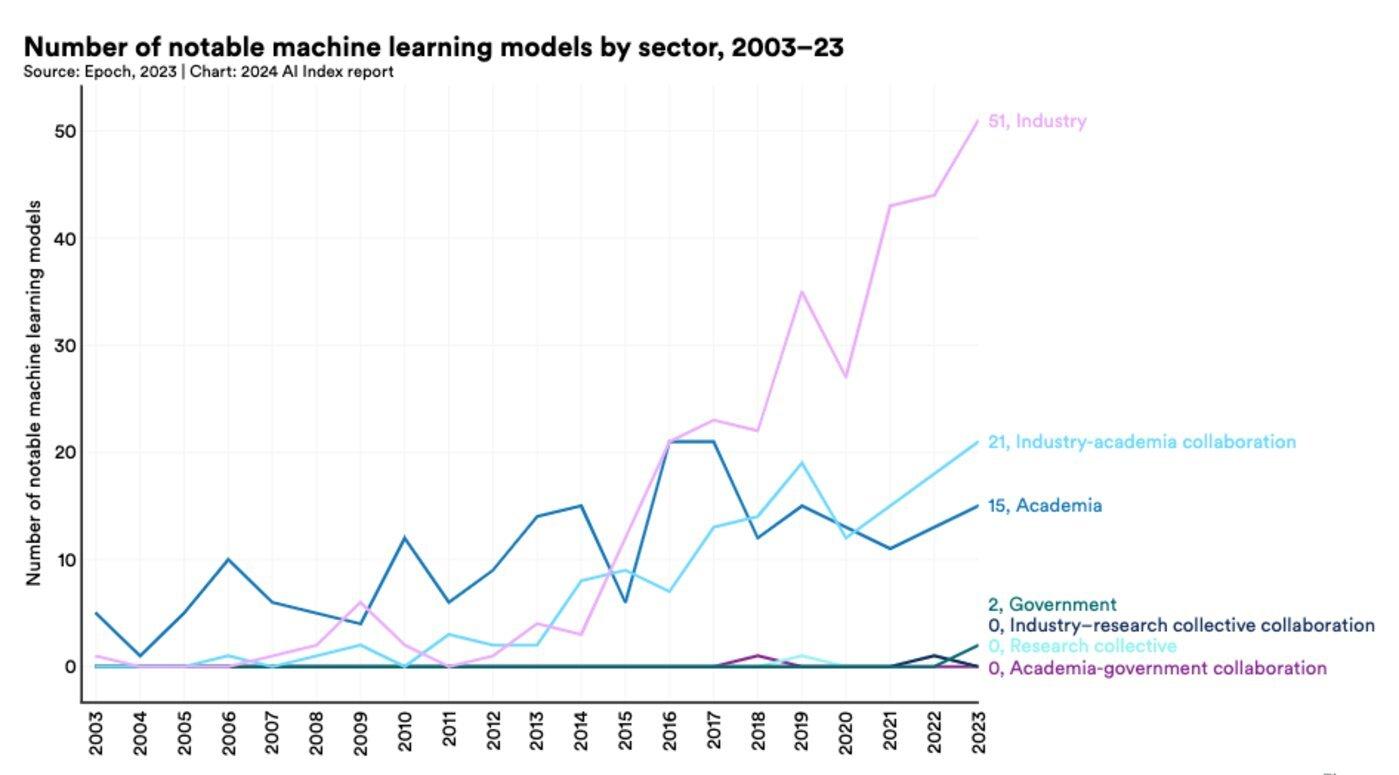

2. Industry continues to dominate frontier AI research.

A total of 51 notable machine-learning models were produced by industry, while academia produced just 15. However, a record-high 21 models came from industry-academic collaboration.

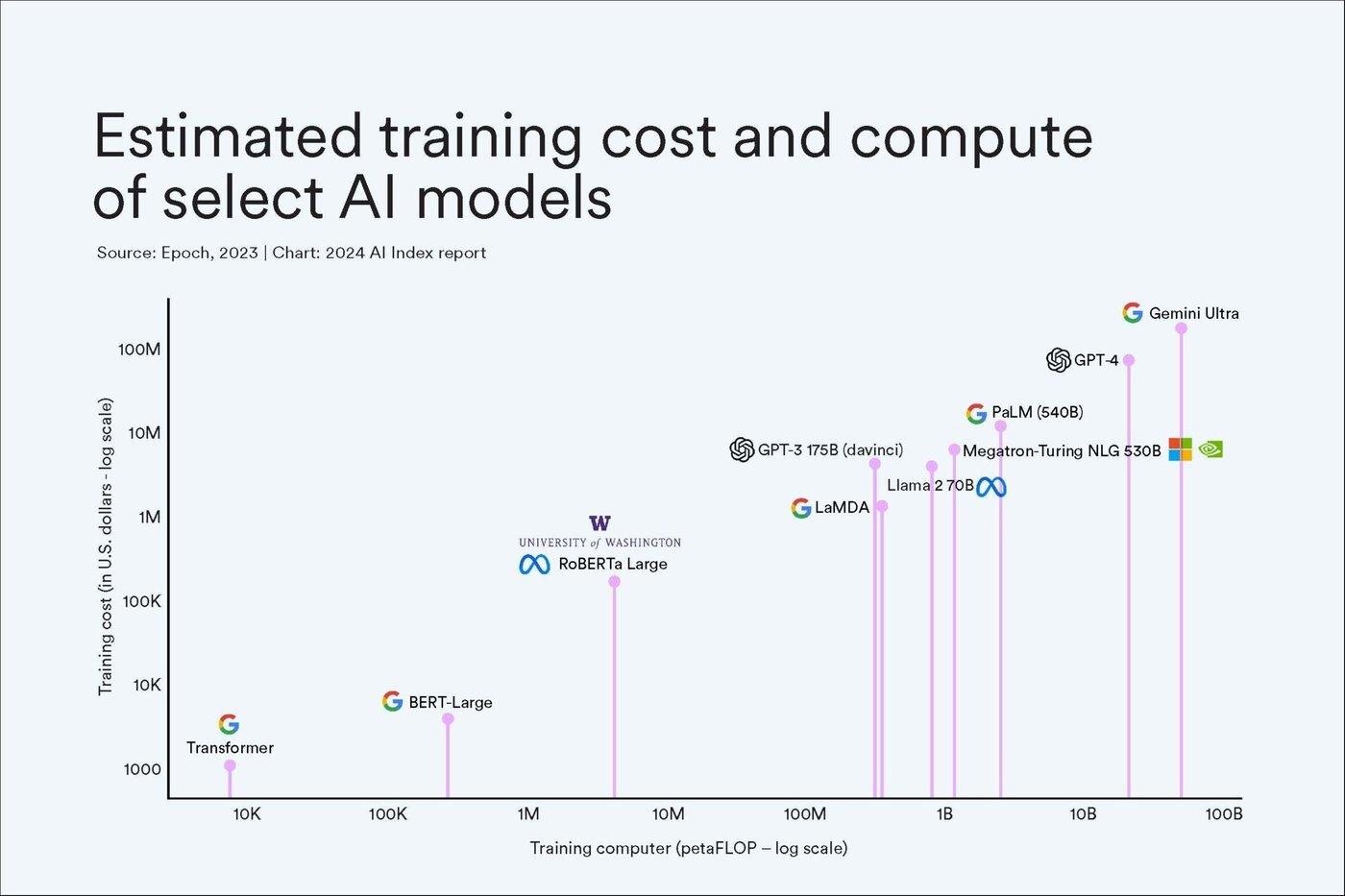

3. Frontier models get way more expensive.

Training costs for state-of-the-art AI models are unprecedented. Examples given are the estimated $78m of compute used for OpenAI’s ChatGPT, and $191m for Google’s Gemini Ultra.

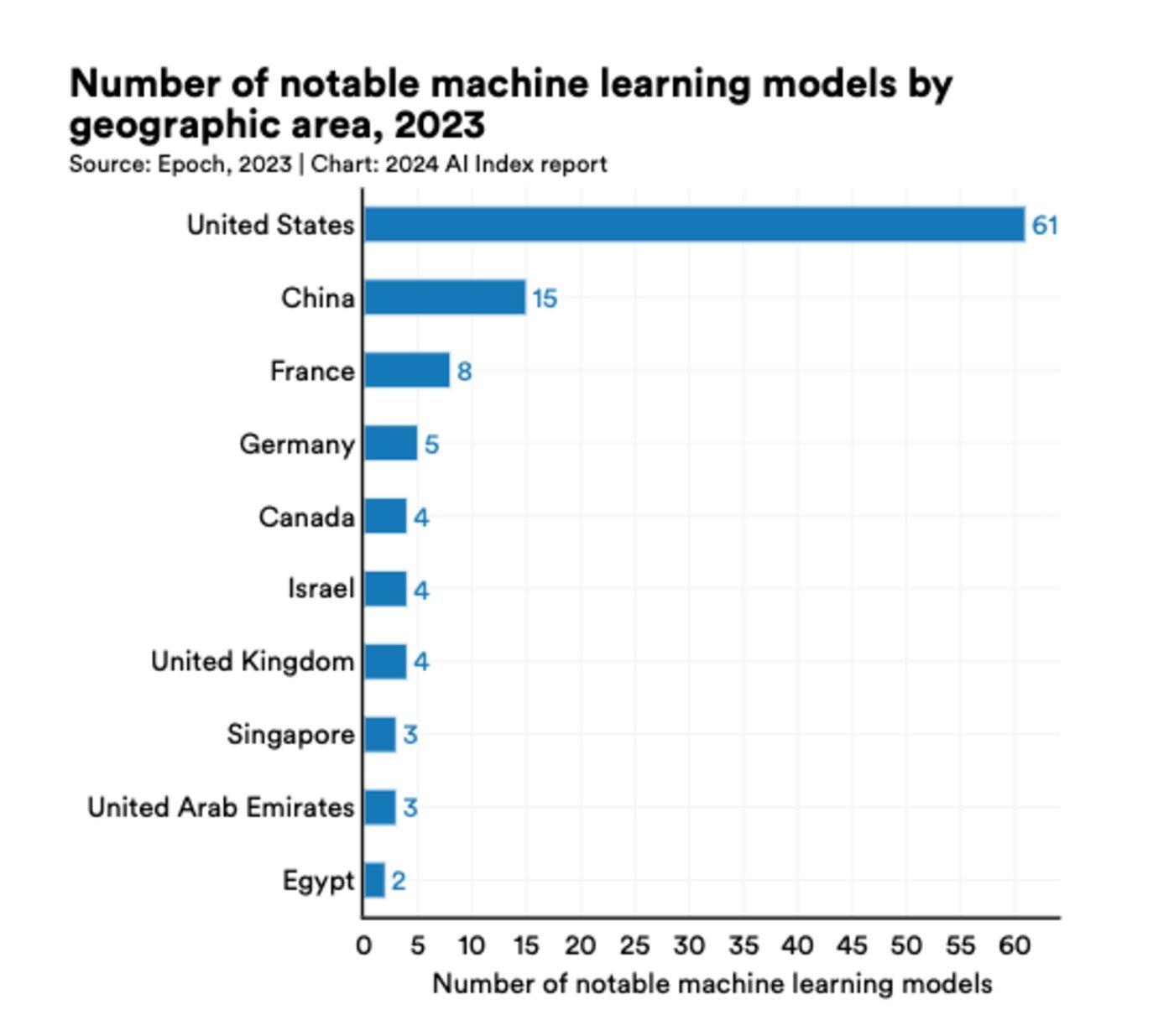

4. The United States leads China, the EU, and Britain as the primary source of top AI models.

Institutions in the U.S. were responsible for originating 61 notable AI models during 2023, with 15 from the EU and 12 from China.

5. Robust and standardized evaluations for LLM responsibility are seriously lacking.

AI Index research revealed “a significant lack of standardization in responsible AI reporting”. Leading developers such as OpenAI, Google and Anthropic all primarily test against different benchmarks.

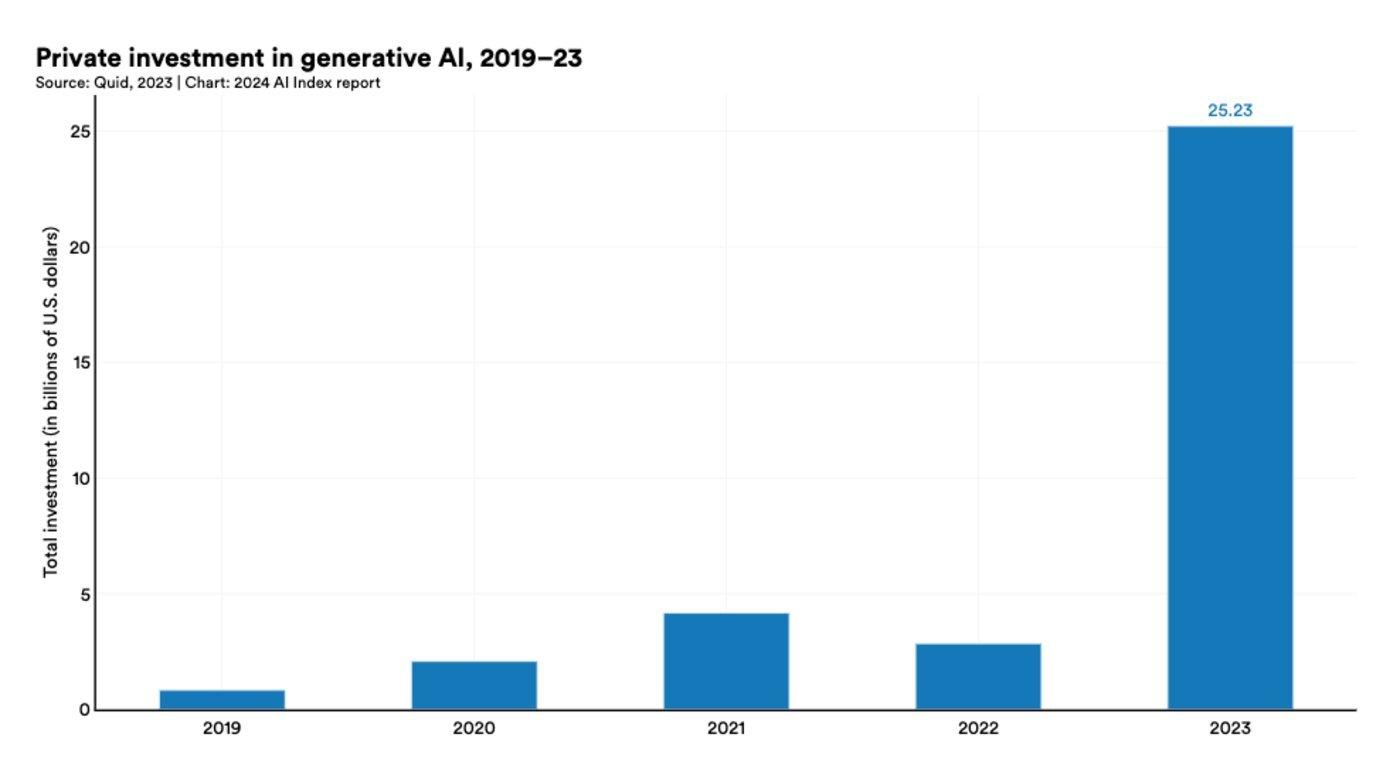

6. Generative AI investment skyrockets.

Despite a decline in overall AI private investment last year, funding for generative AI surged, nearly octupling from 2022 to reach $25.2 billion. Major players in the generative AI space, including OpenAI, Anthropic, Hugging Face, and Inflection, reported substantial fundraising rounds.

7. The data is in: AI makes workers more productive and leads to higher quality work.

Multiple studies revealed that “AI enables workers to complete tasks more quickly and to improve the quality of their output,” and that it bridges the skill-gap between low- and high-skilled workers. But those studies also found evidence that “using AI without proper oversight can lead to diminished performance”.

8. Scientific progress accelerates even further, thanks to AI.

AlphaDev, which makes algorithmic sorting more efficient, and GNoME, which facilitates the process of materials discovery were cited as two of the most significant science-related applications launched thanks to AI.

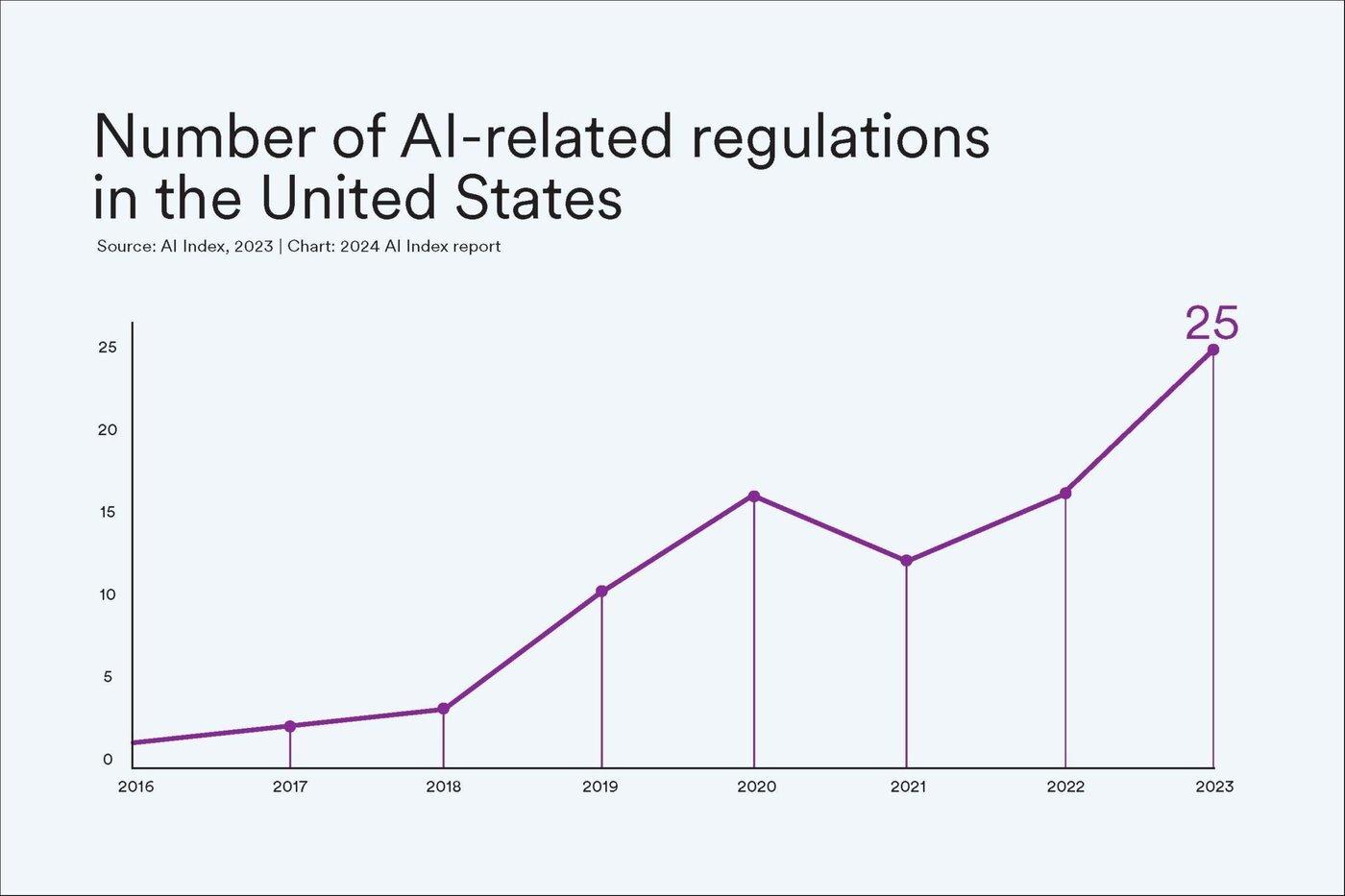

9. The number of AI regulations in the United States increases sharply.

In 2016, there was a single AI-related regulation in the U.S. By 2023, there were 25, a rise of 56.3% from the number in 2022.

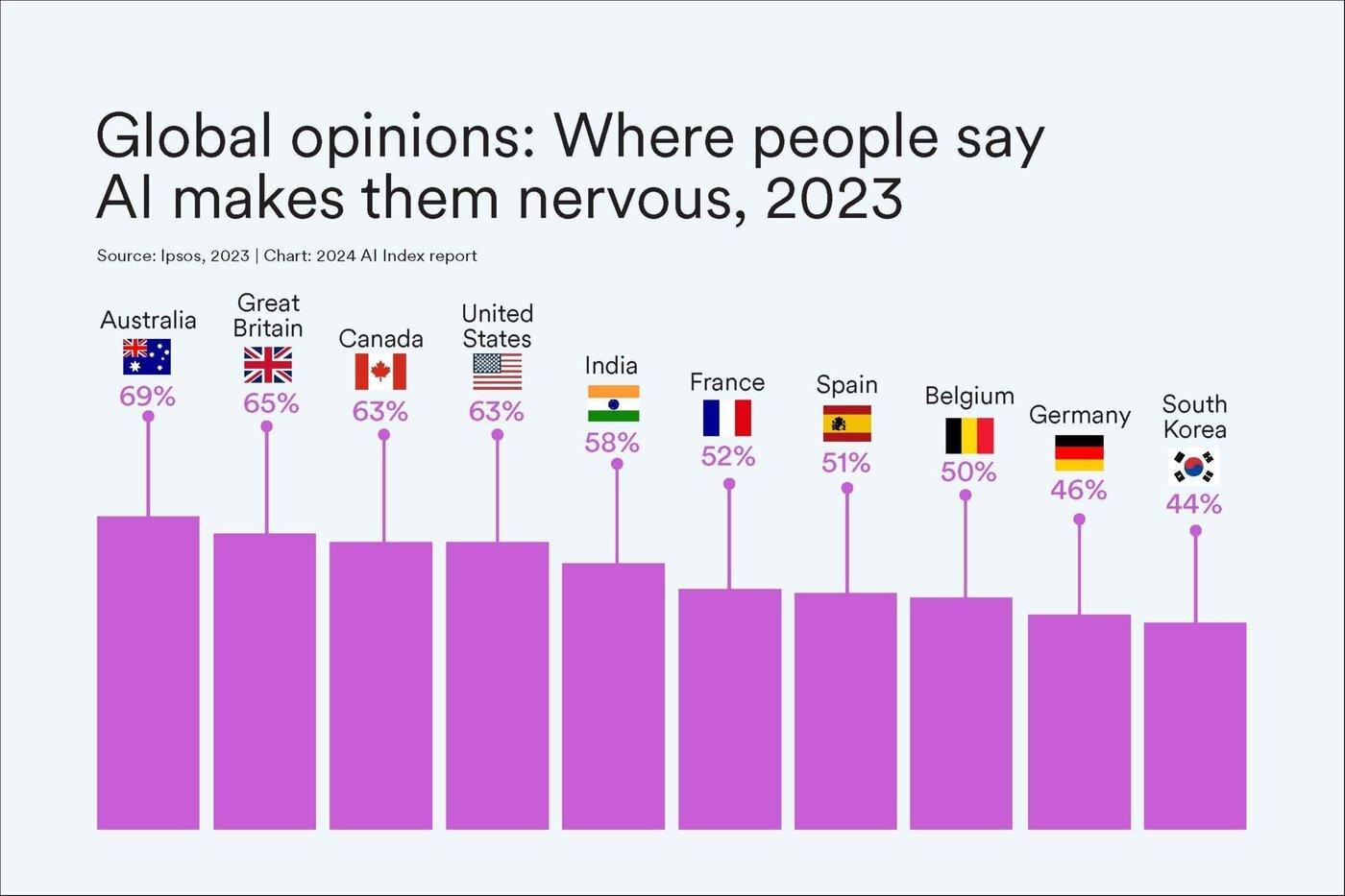

10. People across the globe are more cognizant of AI’s potential impact – and more nervous.

Polling company Ipsos found 66% of people think AI will “dramatically affect” their lives within five years, a rise of 6% on previous polling, while 52% are nervous about AI products and services, up 13%. Pew research in the United States also found more than half those surveyed, 52%, were more concerned than excited about AI.

In the global arena of AI competition, China and the United States emerge as the most prominent contenders, with each wielding distinct advantages across various AI domains.

As per the report, the United States surged ahead in AI large models, boasting a tally of 61 releases in 2023. This figure far surpassed the EU's 21 and China's 15, firmly establishing the United States as the primary source of top-tier AI large models worldwide.

Moreover, the United States maintains a commanding lead in basic model development. In 2023 alone, the country unveiled 109 basic models, dwarfing China's count of 20 by more than fivefold.

In the domain of AI investment and financing, the United States holds a decisive edge. The AI industry investment in the United States soared to $67.2 billion in 2023, a staggering 8.7 times higher than China's $7.8 billion, the second-largest investor. While China and the EU witnessed declines of 44.2% and 14.1%, respectively, in private AI investments since 2022, the United States experienced a significant 22.1% upswing during the same period.

Over the decade spanning from 2013 to 2023, the United States accumulated a total AI investment of $335.2 billion, trailed by China at $103.7 billion.

The disparity between China and the United States is even more pronounced in private investment in generative AI. In 2023, the total investment in generative AI in the United States stood at $22.46 billion, compared with China's meager $0.65 billion.

In terms of the sub-domains of private AI investment, the top three areas in 2023 were AI infrastructure/research/governance ($18.3 billion), NLP and customer support ($8.1 billion), and data management and processing ($5.5 billion).

While the United States dominates investment in AI infrastructure/research/governance, China outstripped the United States in facial recognition investments in 2023 ($130 million vs. $90 million). Similarly, in the semiconductor sector, China's investment ($630 million) nearly rivaled that of the United States ($790 million).

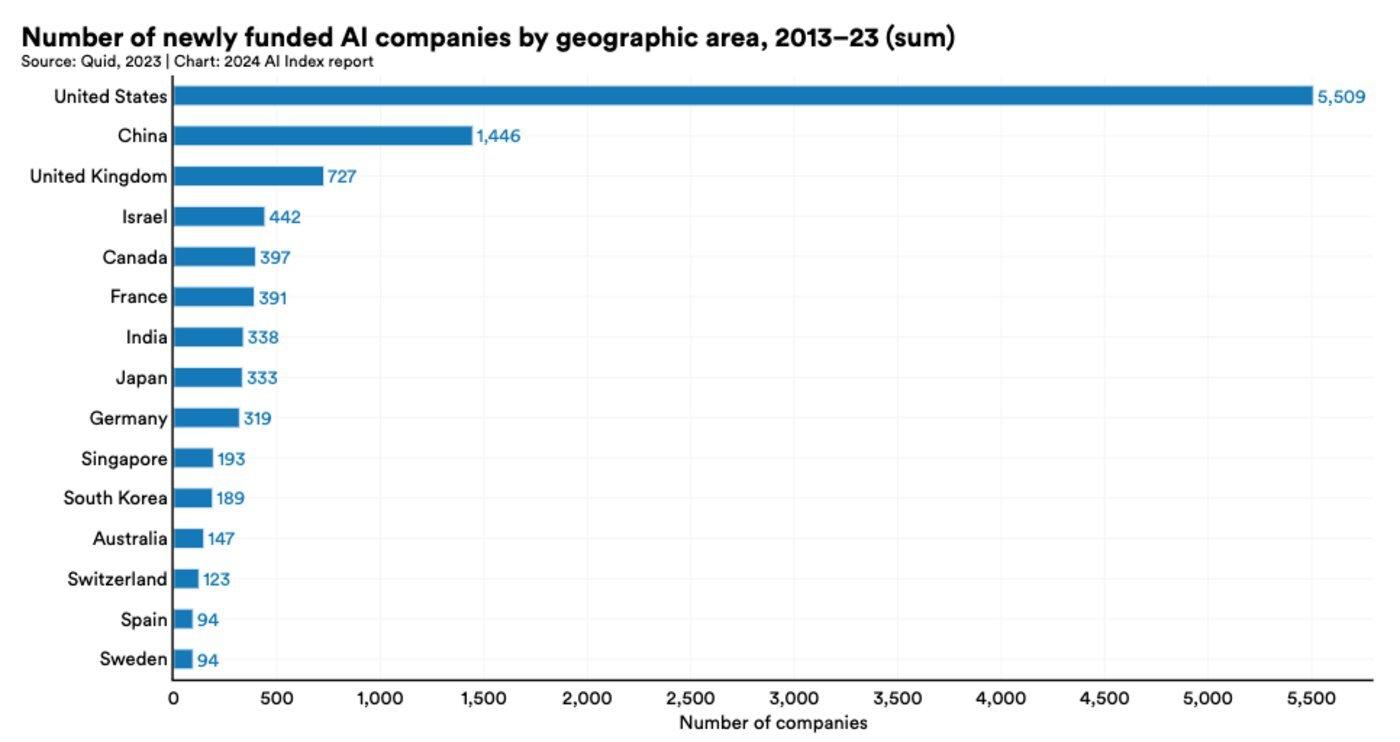

In 2023, the United States boasted 897 successful financing for AI startups, compared to China's mere 122. Over the past decade (2013-2023), the United States announced successful financing for 5,509 AI startups, a figure 3.8 times higher than China's 1,446.

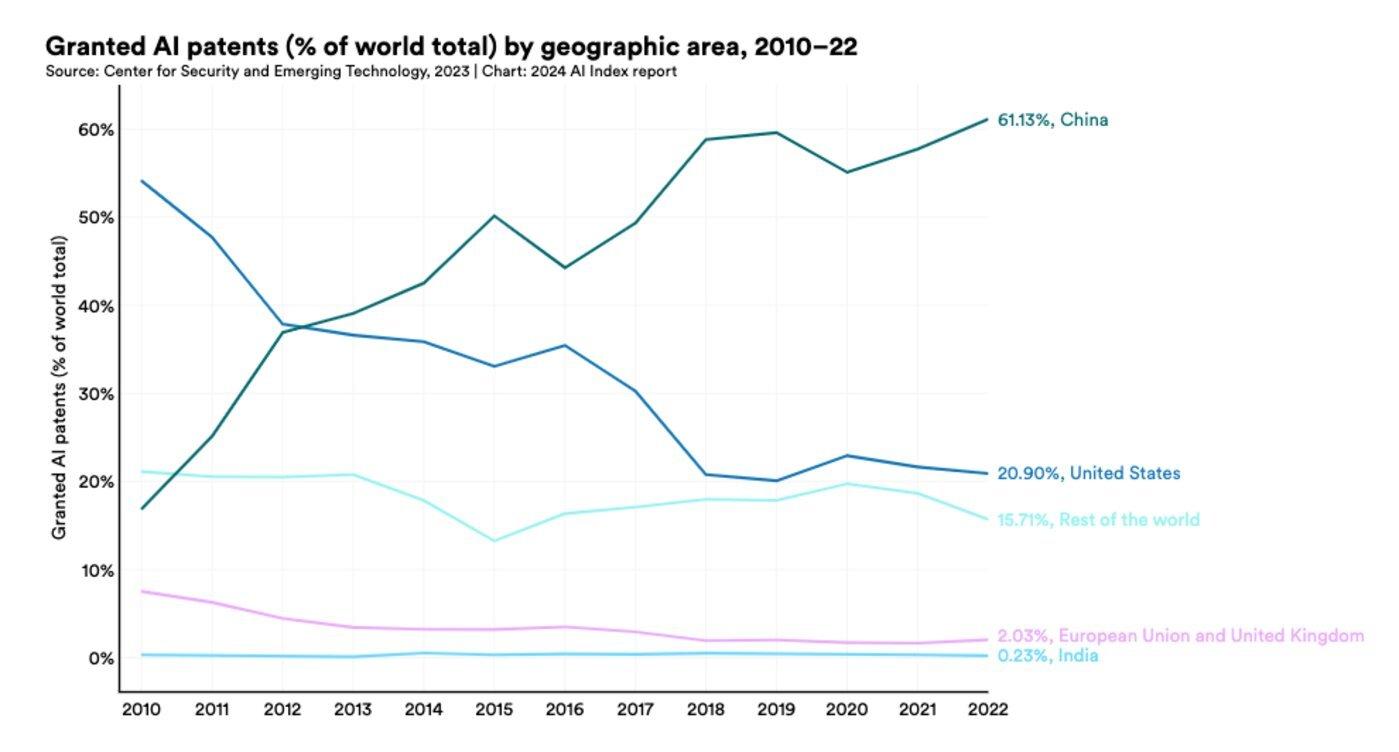

Despite the United States' dominance in basic model research and AI investment and financing, China holds sway in global AI patent quantity and industrial robot installations.

From 2021 to 2022, global AI patents granted surged by 62.7%, while China's share hit 61.1% in 2022, far surpassing the United States' 20.9%.

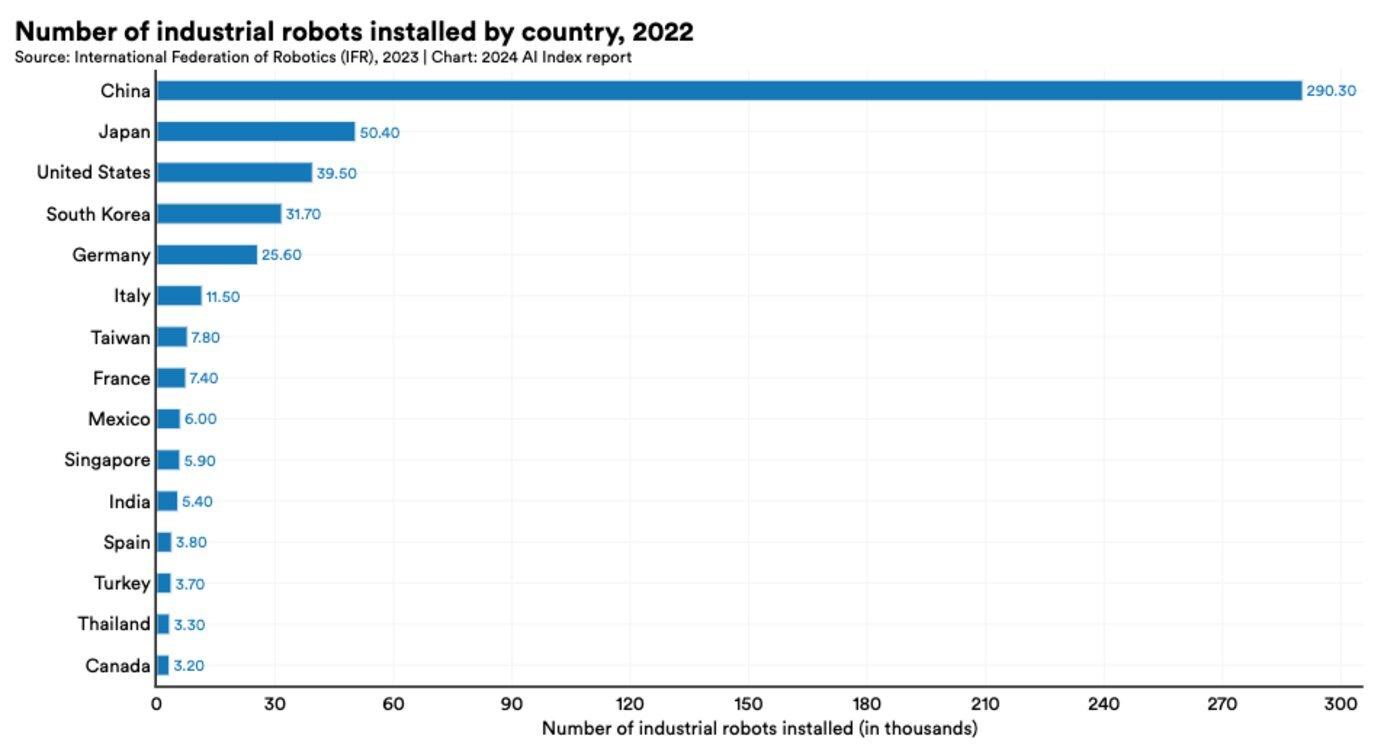

China's demand for industrial robots has surged over the past decade, with its global share of installations skyrocketing from 20.8% in 2013 to 52.4% in 2022, securing the top spot globally.

In 2022, China installed 290,300 industrial robots, a figure 7.4 times higher than the United States' 39,500. The electrical/electronics industry led in industrial robot installations in China, followed by the automotive and metal/mechanical industries.

In contrast, the United States dominates professional service robot manufacturing, boasting 218 manufacturers, approximately double that of China's 106.

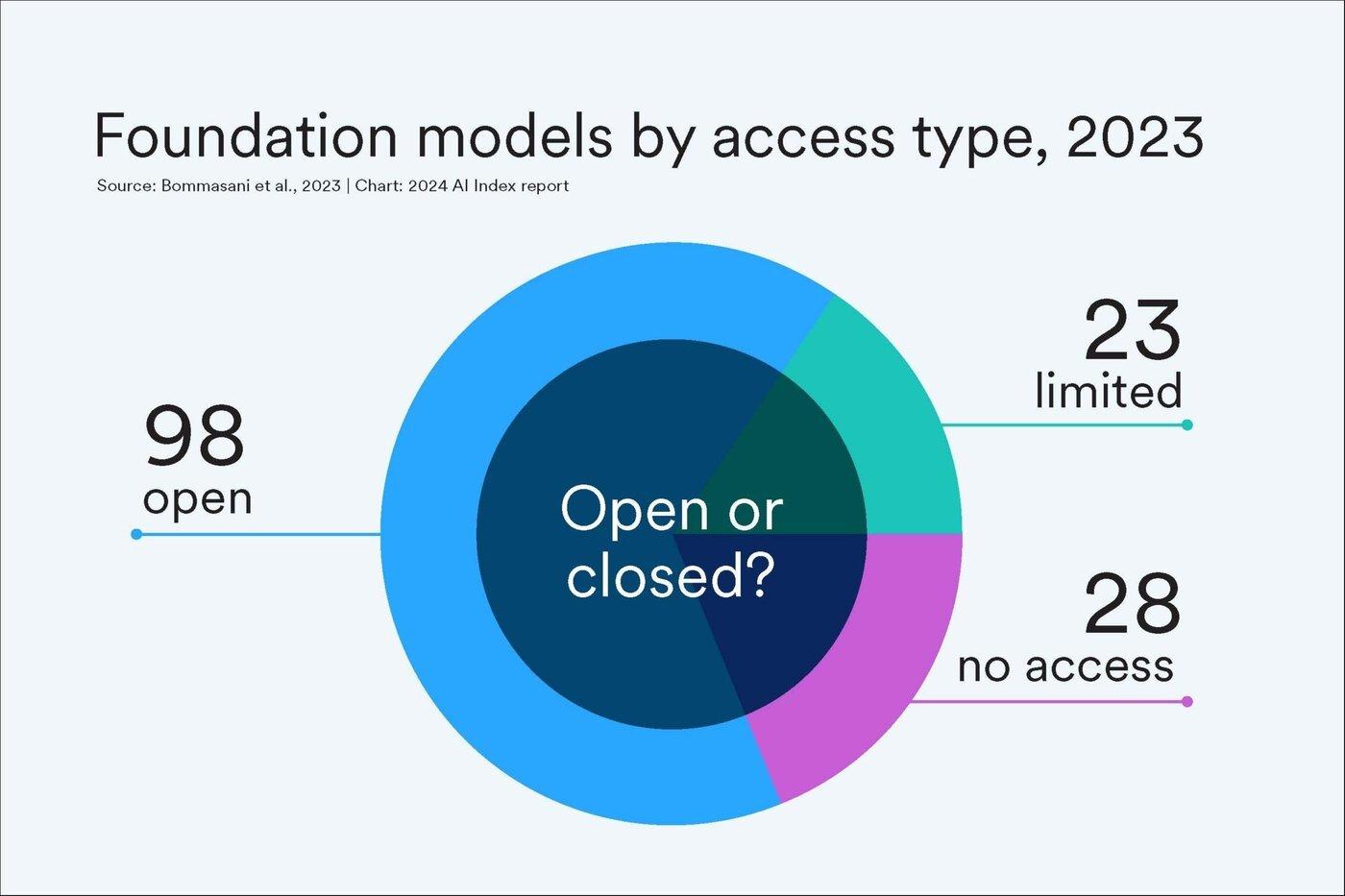

Furthermore, closed-source large models outshine open-source ones, with Google leading the pack in model releases. In 2023, Google unveiled 18 large models, including Gemini and RT-2, surpassing Meta and Microsoft, which released 11 and nine large models, respectively.

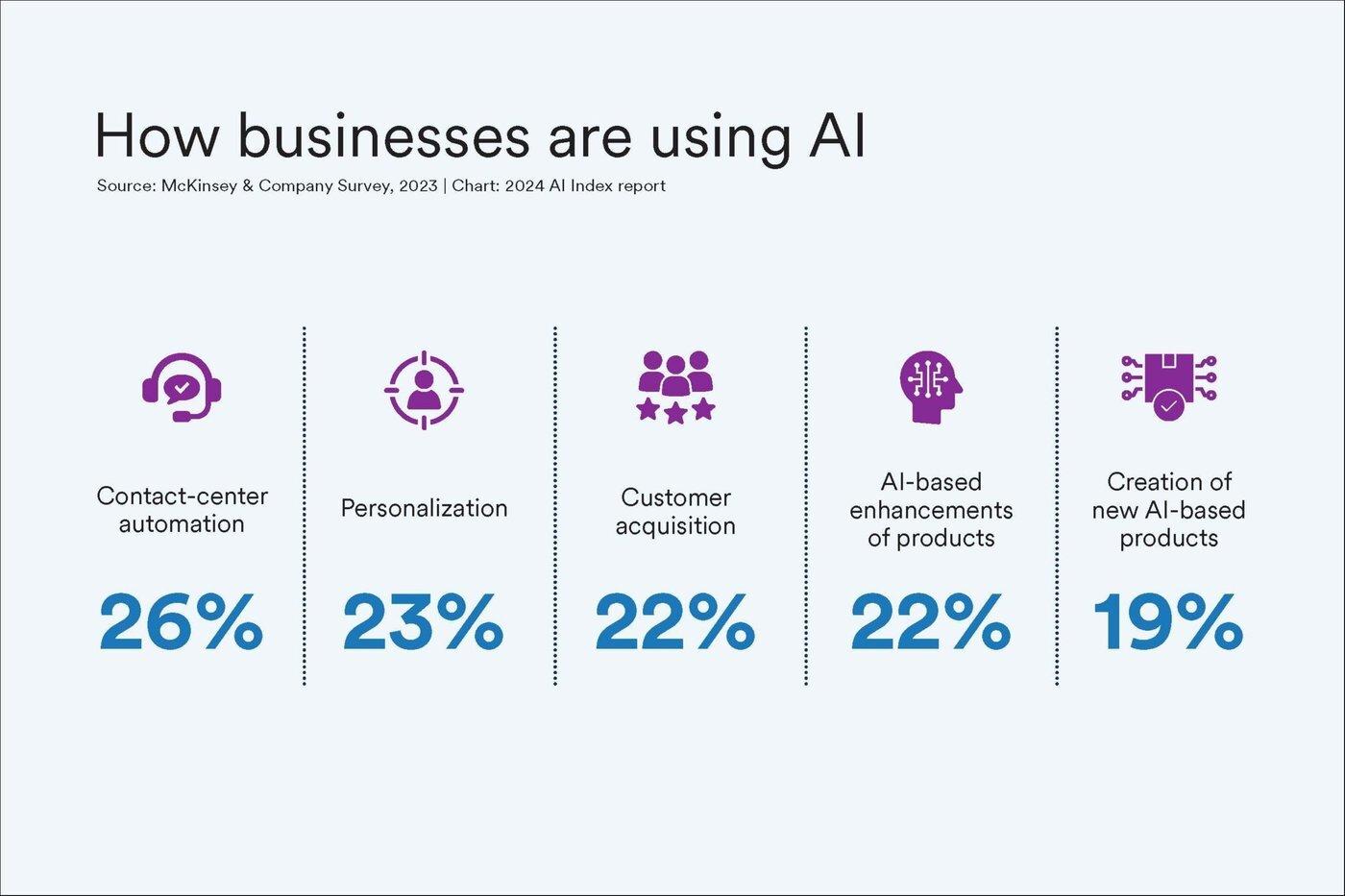

As more companies harness AI to bolster their operations, the report reveals a rising adoption rate, with 55% of organizations utilizing AI in 2023, compared to 50% in 2022 and 20% in 2017. AI applications primarily center around automated contact centers, personalized content, and customer acquisition.

A global survey conducted by the AI Index highlights widespread beliefs regarding AI's impact on employment. In particular, 66% of Generation Z and 46% of Baby Boomers anticipate significant effects on their current jobs. Respondents with higher income, education levels, and decision-making roles anticipate substantial employment impacts.

Concerns about the impact of AI products and services on the job market vary by country, with 69% of Australians and 65% of Britons expressing unease. By comparison, Japan exhibits the lowest level of concern at 23%.

Despite public apprehensions about AI's impact on jobs, a Goldman Sachs report cited by the AI Index forecasts a 1.0% to 1.5% annual productivity growth increase globally over the next decade.